Factor investing #2: Addressing factor gaps or tilts

This is the second in a series of articles compiled by Jason Swartz – a member of the team at our partner Satrix – that unpack the concept of factor investing and how it’s used in different situations. (Here’s last week’s article: Understanding what drives performance in your portfolio) We will continue publishing an article a week on our blog for the next several weeks.While these articles are aimed at institutional investors, the content is still relevant – and interesting – for individuals who like to know what happens in the background, or who have their own factor investment strategies in place.

Factor investing is one of the tools used by portfolio managers to maximise returns in an investor’s portfolio. Factors employed vary from portfolio to portfolio and from manager to manager. A momentum strategy, for example, focuses on trends in share prices, whereas a value investor would look specifically for shares that he or she believes to be undervalued in the market. More definitions are available here.

This week’s article explains how to address factor gaps or tilts in your portfolio.

Address factor gaps or tilts in your portfolio

By Jason Swartz, Satrix

Client level of adoption/allocation:

Factor investing has the ability to er consultants, multi-managers and advisors to build client portfolios of sIn licity, from ‘not allocating’ to ‘sophisticated allocation’. In this series we aim to highlight all applications of tor investing across this continu

In the first article in our series on factor investing we explained what these factors are. We also touched on how you could use factor investing to break down where the performance of your portfolio comes from and evaluate how much alpha – outperformance – your active manager is really adding.

In part 2 of this series we take the next logical step: we discuss how you can do something about those factor exposures. This concept is typically referred to as ‘portfolio completion’.

As the word suggests, portfolio completion is the exercise of adding or reducing specific exposures to your portfolio to fill a gap and achieve a targeted portfolio strategy. This step usually involves only a minor allocation to a factor, but is vitally important to address your specific investment needs appropriately.

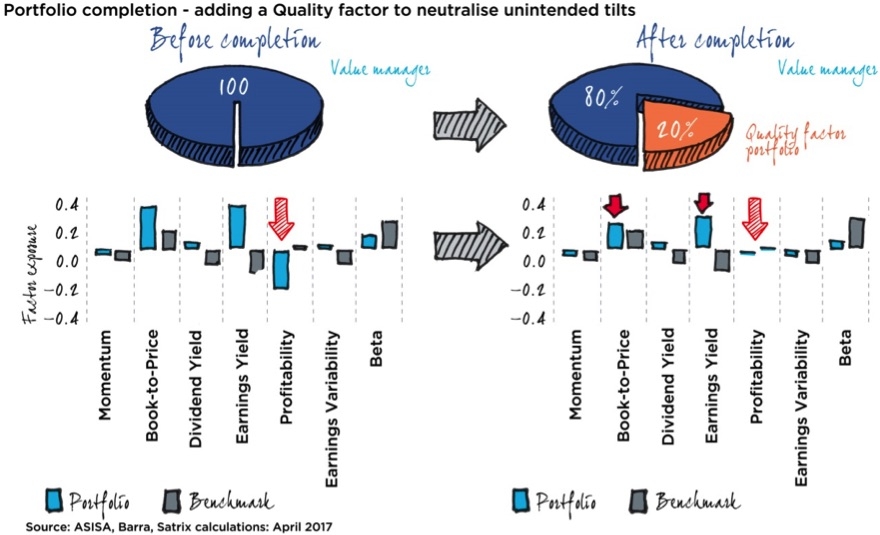

Let’s take an example of an equity value manager. After examining the portfolio’s factor exposures relative to the benchmark, we observe a significant underweight in the profitability factor exposure:

Since most factors are not free from exposure to the others (styles overlap), it is likely that while trying to gain exposure to certain targeted exposures, other undesired factor exposures may creep in. And while perfectly disentangling these factors is not always realistic, it would make sense to at least neutralise these unintended exposures. This should ensure that the portfolio achieves enhanced purity in the targeted exposures as well as mitigating any meaningful portfolio risks through unintended factor exposures.

In our example, while targeting a Value strategy (particularly if shaped around a dividend yield factor), an unintentional but significant consequence is an underexposure to profitability. Profitability, being a factor within the Quality family of factors, has proven to be one of the most consistently strong factor signals in South Africa. As such, being meaningfully underexposed to this factor may compromise the premium added by the targeted Value factor. The objective then is to neutralise the profitability exposure by adding a small allocation (20%) to Quality, while not substantially diluting the intended Value exposure. We achieved this in our example.

What we’re trying to achieve here is the best balance between diluting the desired factor exposures and enhancing the diversification of the fund. This trade-off exists due to the factor used for completion (Quality) often being somewhat negatively correlated with the existing portfolio (Value).

Portfolio completion offers the added bonus of better portfolio diversification, while the investor can also leave the active manager to continue with its specific style and thereby not constrain its process.

In the video below Jason Swartz from Satrix discusses how to change unintended factor tilts or gaps in a portfolio.

Factor investing #4: Blending risk factors and styles

This is the fourth in a series of articles compiled by Jason Swartz – a member of the team at our

Factor investing #7: Environmental, social and governance considerations

This is the seventh article in our series on factor investing, compiled by Jason Swartz of Satrix

Factor investing #1: Understanding what drives performance in your portfolio

This is the first in a series of articles compiled by Jason Swartz – a member of the team at our p